The true cost of PPO participation isn’t the 30-60% fee cut you see on every explanation of benefits. It’s closer to 70-80% of what you should be earning, once the hidden costs surface.

That’s the answer most dental consultants won’t give you straight.

Here’s what that looks like in real life.

You know that “successful” practice down the street? The one seeing 40 patients a day, booked solid for months, three hygienists running flat out? The owner is going broke.

I know, because I’ve seen the books.

Revenue looks great on paper: $1.8 million a year. Impressive, right?

Except after PPO write-offs, administrative drag, and the hamster wheel of volume care, that owner took home less than most of his staff did last year.

He’s not alone. And neither are you.

This piece breaks down where your money actually goes, why that “steady” stream of PPO patients is quietly draining your practice, and how the dentists who figured this out now work fewer hours for more profit.

First, let’s kill the biggest lie in dentistry: that you need PPOs to survive.

You don’t. They need you.

And they’re getting rich while you stay busy.

Table of Contents

The PPO Lie Everyone Believes

Walk into any dental practice and ask the owner why they participate in PPO networks. You’ll hear the same script every time:

“PPOs bring me steady patients.”

“I need the patient flow.”

“It’s predictable income.”

“Everyone else is doing it.”

Every word is a lie. Not on purpose. These dentists believe what they’re saying.

But it’s still wrong.

Why PPO’s Don’t Bring You Patients

PPOs don’t bring you patients. They bring you customers. There’s a massive difference.

Patients choose you because they trust your expertise, value your care, and want the best treatment available. Customers choose you because their insurance card works at your office.

Guess which one vanishes the second you’re not the cheapest option on their plan?

Loyalty vs. Convenience: The Fatal Mistake

That “steady flow” you’re so grateful for? It isn’t loyalty. It’s convenience.

And convenience is the enemy of profitability.

The “predictable income” myth is even more dangerous. Yes, you can predict you’ll be busy. You can also predict you’ll work twice as hard for half the profit.

That’s not predictable income. That’s predictable burnout.

Why “Predictable Income” Is a Dangerous Myth

Here’s the part that should really bother you. While you’re grateful for the “opportunity” to join their network, PPO companies are using your fear against you.

They know you believe you need them more than they need you.

So they squeeze. Every year, a little tighter:

- Fee reductions disguised as “market adjustments”

- New administrative requirements that cost you time and money

- Delayed payments that choke your cash flow

- Treatment limits that turn you into a technician instead of a doctor.

You’re not building a practice. You’re running an insurance processing center that happens to have dental chairs.

And the real gut punch? Most PPO dentists trade dollars for pennies and call it good business. They stay so focused on being busy that they never stop to calculate what busy actually costs them.

It’s time to change that conversation.

Direct Financial Hits: The Numbers That’ll Make You Sick

Let’s talk about money.

Real money.

Not the fake revenue numbers you tell yourself make PPO participation worthwhile.

Crown Example: The True Cost of PPO

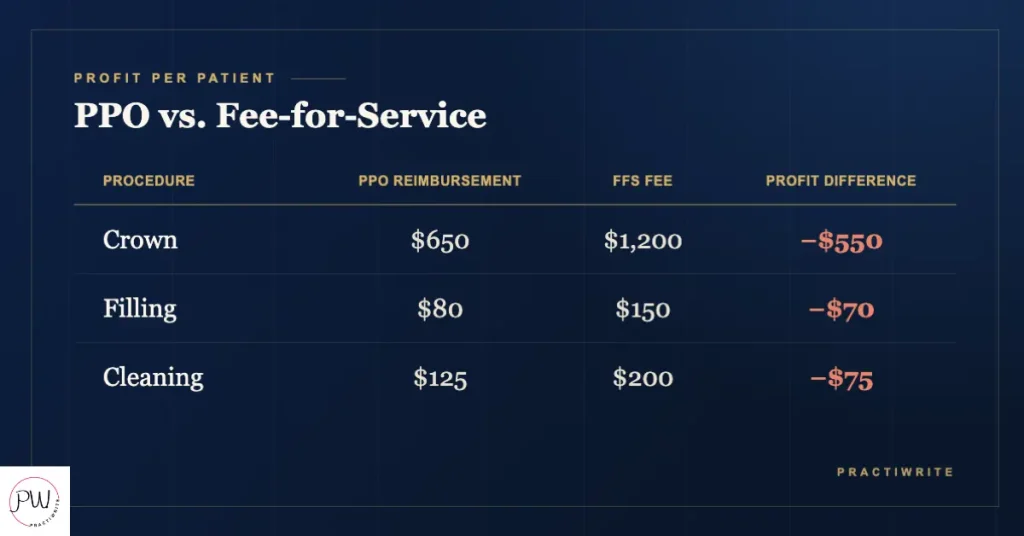

You think you understand PPO costs because you see the fee cuts. Your $1,200 crown becomes $750 with Delta Dental. Your $200 cleaning drops to $125 with MetLife. You call it a 30-40% reduction and tell yourself it’s the cost of doing business. You’re wrong. And that mistake costs you hundreds of thousands every year.

Here’s what actually happens when you accept that PPO crown:

- Your fee: $1,200

- PPO allowable: $650 (a 46% cut)

- Your lab bill: $200

- Staff time (2 hours at $30/hour): $60

- Materials and overhead: $140

- Total costs: $400

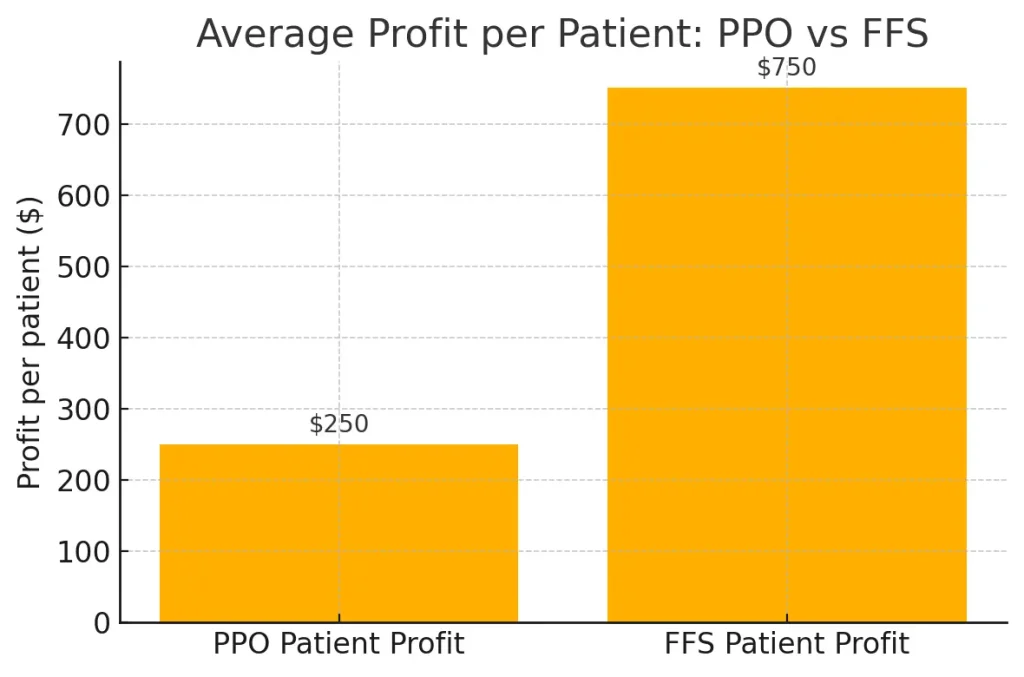

- Your actual profit: $250

But it gets worse.

Your fee-for-service patients would have paid the full $1,200, leaving you $800 in profit. So you didn’t just lose $550 in revenue. You lost $550 in profit potential.

Now multiply that across every PPO procedure you do. For a practice doing 500 crowns a year, that’s $275,000 in lost profit. Annually. Just on crowns.

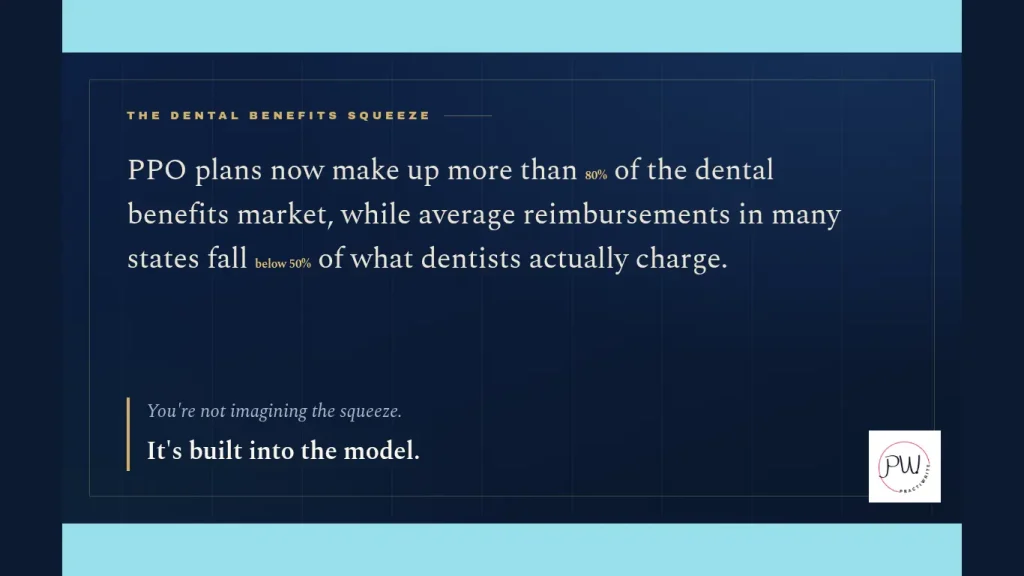

And crowns aren’t the only procedure getting gutted. Every root canal, every bridge, every filling gets the same treatment. Factor in everything and most PPO practices write off $400,000 to $600,000 a year compared to fee-for-service rates.

Still think that 30-40% reduction isn’t so bad?

The $6.2 Million Wake-Up Call

Here’s the math that should keep you up at night. If you’re writing off $500,000 a year, and PPO contracts typically build in 2-3% fee cuts annually, you’re not just losing half a million this year. Over the next decade, assuming a modest 3% inflation and 3% annual PPO cuts, your total lost revenue tops $6.2 million.

Six. Point. Two. Million. Dollars.

And that’s just the visible money. It doesn’t count the lab that won’t give you PPO discounts, the rent that doesn’t care about your write-offs, or the staff salaries that keep climbing while your per-procedure revenue keeps falling.

One practice owner in Texas pegged his annual PPO write-offs at $540,000. His fixed costs? $480,000. He was working for free eleven months out of the year just to break even.

The twelfth month, if he was lucky, was his actual profit.

This isn’t sustainable. It isn’t even rational. But millions of dentists do it every single day, telling themselves they run successful practices while they slowly go broke.

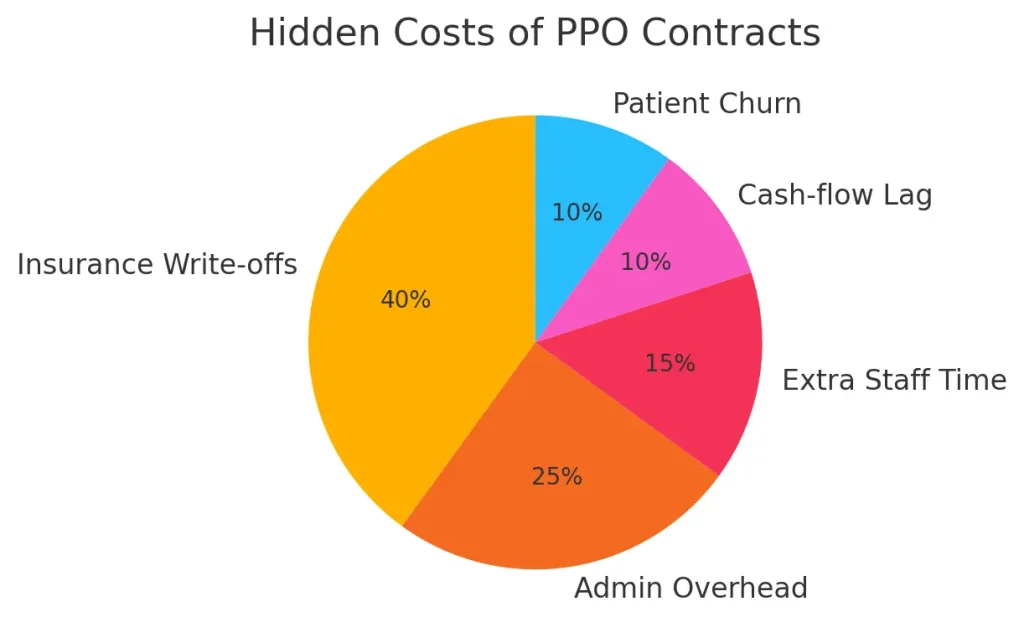

Hidden Costs That Are Killing You Slowly

The fee cuts are just what they want you to see. The real drain happens in the shadows. Death by a thousand administrative cuts that most dentists never bother to calculate.

You know that sinking feeling when your front desk says they spent three hours on hold with Cigna yesterday? That’s not just frustrating. That’s $90 in lost productivity.

Multiply it by every insurance hassle, every week, and you’re looking at $15,000 to $20,000 a year in phone time alone. And phone calls are the easy part.

Administrative Hell: Phones, Pre-Auths, Denials

Pre-authorization is where practices go to die. Every major procedure needs approval from someone who’s never held a dental instrument.

Your treatment coordinator spends 30 minutes documenting, submitting, and following up on each request. At $25 an hour, that’s $12.50 per pre-auth. For a practice doing 200 major procedures a year, that’s $2,500 just in submission time.

Then they deny 40% on first submission. Now you’re filing appeals, gathering documents, making calls. What started as $12.50 becomes $45 to $60 per approved procedure.

And some never get approved at all.

One client in Ohio tracked this for six months. This practice spent 127 hours on pre-authorizations that produced $89,000 in approved treatment. Cost of those hours: $3,175.

But here’s the gut punch. They also spent 73 hours on denials and appeals that produced zero revenue. Total administrative cost: $5,000 to collect $89,000. And that’s before we talk about claims processing.

Claims Processing Costs: Time and Trust Lost

PPO practices see 15-25% initial claim denial rates. Every denial triggers a 20-30 minute investigation:

- Was it coded wrong?

- Missing documentation?

- A coordination-of-benefits issue?

Your staff turns into insurance detectives instead of the people who help patients say yes to care.

The hidden cost here isn’t just time. It’s opportunity. Every hour spent fighting insurance is an hour not spent on treatment planning, patient education, or work that actually generates revenue.

It’s an hour not spent making your practice better.

Technology costs pile on top. PPO contracts demand specific software, regular updates, and compliance monitoring. You’re paying for systems to manage relationships that are costing you money.

It’s like buying the rope to hang yourself.

Staff Turnover: Burnout by Insurance

Staff turnover speeds up under PPO pressure. When your team spends half the day on insurance bureaucracy instead of helping patients, they burn out. Fast.

The average cost to replace a dental team member runs about $75,000 once you factor in recruitment, training, and lost productivity. High-performing practices lose 2-3 team members a year to PPO burnout.

That’s $150,000 to $225,000 in turnover costs.

Every year.

Forever.

Case Study: $241K in Hidden Costs

Here’s a real one. A practice in Phoenix tracked every PPO-related administrative cost for 12 months. The results were nauseating:

- Phone time with insurance: $18,500

- Pre-authorization processing: $21,000

- Claims management and appeals: $31,000

- Additional software and compliance: $12,500

- Extra training for constant rule changes: $8,000

- Turnover costs (2 team members): $150,000

- Total hidden costs: $241,000

That’s nearly a quarter million in costs that never show up on your P&L as “PPO expenses.” They’re buried in payroll, scattered across overhead, invisible until you actually add them up. This practice was already writing off $420,000 in direct PPO fee cuts.

Add the hidden costs and the total annual PPO expense hit $661,000. For a practice grossing $1.4 million, that’s 47% of revenue going to subsidize insurance companies.

And it gets worse every year.

The Volume Trap: Why Seeing More Patients Makes You Poorer

Here’s where most dentists make their fatal mistake. PPO margins are thin, so the obvious fix seems to be volume:

- See more patients.

- Book tighter.

- Add evening hours.

- Work Saturdays.

- Pack the operatories like sardine cans and make up thin margins with higher patient counts.

It’s logical. It’s also financial suicide.

Why More Patients = Less Profit

The volume game is rigged against you from the start. Every extra patient you squeeze in costs you money in ways you’re probably not counting.

Start with the obvious: rushed care kills case acceptance. When you’re booking 8-minute exams because you need to see 35 patients a day, you’re not doing comprehensive dentistry.

You’re doing screening exams. You miss opportunities. You rush diagnoses.

You can’t build the relationships that lead to treatment acceptance.

Case Acceptance Plunge from Short Visits

Fee-for-service practices average 60-80% case acceptance on treatment plans over $1,000. PPO volume practices? 30-40%.

When you rush patients through like cattle, they feel it. They don’t trust rushed recommendations. They postpone treatment. They get second opinions elsewhere.

One practice tracked this religiously. When they cut hygiene appointments to 12 minutes, case acceptance dropped 23% compared to 15-minute visits. The time saved: three minutes per patient. The revenue lost: $180,000 a year.

And case acceptance is just the start of the volume death spiral.

Burnout and Equipment Breakdown

Your team burns out faster running between operatories all day. Stressed teams make more mistakes. More mistakes mean more redo work, more complaints, more time managing problems instead of delivering care.

Soon, you’re working harder just to hold the quality you used to deliver in your sleep.

Your equipment takes a beating at maximum capacity. That dental chair rated for 8 hours of daily use? You’re pushing it 10-12.

Maintenance costs climb. Equipment fails more often. Downtime becomes a financial disaster when you’re booked solid.

The hidden cost everyone misses? The opportunity cost of the wrong patient mix.

Opportunity Cost of Saying Yes to the Wrong Patient

Every PPO patient in your chair is a fee-for-service patient you can’t see. Every 15-minute, $125 cleaning is a potential $2,000 cosmetic consult you’re turning away. Every rushed crown prep is a full-mouth reconstruction you don’t have time to present.

One of my clients learned this the hard way.

Her practice was seeing 45 patients a day across 8 operatories. Busy as anything, revenue looked good on paper at $2.1 million a year. But when she calculated her true hourly rate, including all the hidden costs of volume, she was making $47 an hour.

Less than her hygienists.

The breaking point came when she realized she hadn’t done a comprehensive exam in six months. Every patient was maintenance or emergency.

No treatment planning. No relationship building. No professional satisfaction.

Here’s the math that changed everything for her. Forty-five PPO patients a day generated an average of $115 profit per patient after all costs. Total daily profit: $5,175.

When she cut back to 25 patients a day and raised her standards, average profit per patient jumped to $280. Total daily profit: $7,000. She made 35% more money working with 44% fewer patients.

The volume trap isn’t just about money. It’s about what kind of dentist you become.

When you chase numbers instead of practicing dentistry, you stop being a healthcare provider and turn into a production machine.

Your satisfaction tanks. Your skills atrophy. Your reputation suffers.

Worst of all, you train your patients to expect rushed, commodity care. They stop seeing you as a professional and start seeing you as a vendor. Once that happens, they’ll leave you for anyone $10 cheaper.

Volume doesn’t solve the PPO problem. It amplifies it.

What You’re Really Losing: The Stuff That Matters

The money is bad enough. But PPO participation costs you things you can’t measure in dollars. Things that matter more than your bank account.

Start with the big one: you’re not practicing dentistry anymore. You’re processing insurance claims that happen to involve teeth.

When did you last recommend the best treatment for a patient without first checking their coverage? When did you last suggest a premium material because it was clinically superior, not because insurance would pay for it? When did you last practice medicine instead of practicing insurance?

PPO Contracts Kill Your Recommendations

PPO contracts don’t just cap your fees. They cap your judgment. You can’t recommend what you know is best because some claims processor in Des Moines decided it’s “not medically necessary.”

You’re not a doctor making medical decisions. You’re a technician following insurance protocols.

That crown that needs replacing? Insurance says it hasn’t been five years, so you wait.

The cosmetic case that would change a patient’s life? Not covered, so you don’t even mention it.

The premium materials that last twice as long? Sorry, insurance only covers amalgam.

You went to dental school to help people. Now you help insurance companies save money by delivering the cheapest acceptable care.

The Value of Your Practice Is Diminishing

Your practice value is getting destroyed in the process. When you sell, buyers don’t just look at revenue. They look at profit margins, insurance dependency, and growth potential.

PPO practices check all the wrong boxes. Comparable fee-for-service practices sell for 20-30% more than PPO practices. If your practice is worth $800,000 as a PPO mill, it could be worth $1.1 million as a fee-for-service practice.

That’s $300,000 you lose at retirement for accepting reduced fees all those years.

Your Quality of Life Takes a Beating

But the real cost is what PPO participation does to your life. Remember why you became a dentist? Probably not to work 60-hour weeks seeing a patient every 8 minutes while drowning in paperwork.

The volume demands mean longer days. The admin burden means working weekends. The financial pressure means you can’t afford the staff or systems that would make life easier.

You’re trapped in a cycle where working more is the only way to hold income, but working more makes you miserable.

One practice owner put it perfectly:

“I was making good money on paper, but I hadn’t taken a real vacation in three years. I was working Saturdays, seeing 40 patients a day, going home exhausted every night. My wife said I’d become a stranger to my own family. What’s the point of a successful practice if it destroys everything else you care about?”

The professional identity crisis runs deeper than most dentists want to admit. You spent eight years becoming a doctor, and PPO contracts reduce you to a commodity provider. Patients don’t choose you for your expertise. They choose you because you’re on their plan.

You’re not Dr. Smith, the skilled restorative dentist. You’re “the guy my insurance covers.” That erodes something fundamental about professional pride.

You stop improving your skills, because insurance doesn’t pay for excellence. It pays for adequacy. You stop investing in advanced training, because patients won’t pay extra for advanced techniques.

You become what your contracts reward: average.

The worst part? It isn’t temporary. Every year you stay in PPO networks, these patterns dig in deeper.

The longer you accept reduced autonomy, reduced income, and reduced satisfaction, the harder it gets to imagine an alternative. You start believing you can’t survive without PPOs.

You convince yourself busy means successful. You accept that tired, frustrated, and financially stressed is just the price of being a dentist. It’s not.

You’re just doing it wrong.

Real Case Study: Dr. Regina’s $920K Annual PPO Cost

A client of mine here in Ohio thought she was running a successful practice. $1.8 million in annual revenue.

Eight operatories. Booked solid for months. Three hygienists at capacity.

By every external measure, she was crushing it. Except she was going broke.

She came to me after her accountant delivered some sobering news: despite record revenue, her practice had made less profit than the year before. Again. For the third year running.

She was working harder, seeing more patients, taking home less. “I don’t understand it,” she said. “We’re busier than ever.”

I understood it perfectly. Regina was trapped in the PPO death spiral and didn’t even know it.

Here’s what her books looked like when we started the audit:

- Annual revenue: $1,800,000

- PPO patient percentage: 85%

- Average daily patient count: 42

- Doctor working hours: 55 per week

Those numbers look impressive until you dig deeper.

The direct hit. Her standard fees totaled $2.34 million a year. Her PPO reimbursements? $1.26 million. Direct write-offs: $540,000. That’s half a million dollars she gave away just to stay “in network.”

And that was only the beginning.

The hidden bleeding. We tracked every PPO-related cost for six months, then projected annually:

- Administrative time (pre-auths, claims, appeals): $89,000

- Extended phone time with insurance: $23,000

- Additional compliance and software: $18,000

- Extra staff training for constant rule changes: $12,000

- Equipment wear from high-volume scheduling: $21,000

- Staff turnover (3 team members that year): $225,000

- Total hidden costs: $388,000

The opportunity cost. This was the killer. Regina was so buried in PPO patients she couldn’t see fee-for-service patients.

We calculated she was turning away roughly $200,000 a year in fee-for-service revenue because she had no chair time.

Total Annual PPO Cost: $920,000

Nearly a million dollars. Gone. For the privilege of being a “preferred provider” for insurance companies slowly strangling her practice.

Regina’s take-home after expenses? $127,000. She was working 55-hour weeks to make less than many of her employees.

“This can’t be right,” she said when I showed her the numbers. It was right. And it was about to get worse, because her PPO contracts included 3% annual fee cuts.

The transformation. Regina and I built an 18-month plan to transition her practice. Not cold turkey, that would have been financial suicide. Systematic, deliberate change.

Months 1 to 6: We dropped the three worst-performing PPO contracts. They represented 15% of her patients but only 8% of her profit. We used the freed capacity to focus on comprehensive treatment planning for the patients who stayed.

Months 7 to 12: We cut two more contracts and started marketing to fee-for-service patients. Regina invested in upgrades, better technology, a stronger patient experience, and staff training in consultative treatment planning.

Months 13 to 18: we terminated the remaining low-performers, keeping only two high-reimbursing plans that delivered genuine value.

The results after 18 months:

- Annual revenue: $1,400,000 (22% lower)

- PPO patient percentage: 35%

- Average daily patient count: 28 (33% fewer patients)

- Doctor working hours: 42 per week

- Take-home profit: $380,000 (a 199% increase)

Read that again. She made $253,000 more per year while working 13 fewer hours per week and seeing 14 fewer patients per day.

Her stress dropped. Her team turnover fell to zero. Patient satisfaction climbed because she finally had time to deliver the care she always wanted to.

“I thought I needed PPOs to fill my schedule. But I was filling my schedule with the wrong patients. I was working twice as hard for half the profit, and I convinced myself that was normal. The scariest part wasn’t losing patients. It was realizing how much of my professional life I’d wasted chasing reimbursements instead of practicing dentistry.”

Regina’s story isn’t unique. It’s just rare that someone actually runs the numbers and has the courage to change course. Most dentists never do the math. They stay busy, stay stressed, and stay broke, convinced they’re successful because their schedules are full. Regina broke free. So can you.

The Compound Effect: How PPO Costs Multiply Over Time

Here’s the part that should worry you most: everything I’ve shown you so far gets worse every single year. PPO contracts aren’t static. They’re built to squeeze harder over time, and most dentists never notice because the strangulation happens slowly.

The Slow Death of Fee Reductions

Every PPO contract includes automatic fee cuts. Usually 2-3% a year, buried in the fine print as “market adjustments” or “fee schedule updates.” You probably signed those clauses without reading them. Most dentists do.

Here’s what that means in real dollars. If you’re writing off $500,000 this year, next year it’s $515,000. The year after, $530,450.

By year five, you’re writing off $562,754 a year. That’s an extra $62,754 in lost revenue from automatic escalations alone.

But inflation doesn’t pause for PPO contracts. Your costs rise 3-4% a year. Rent, salaries, supplies, lab fees, all of it.

Meanwhile, your PPO reimbursements drop 2-3% a year. You’re squeezed from both sides.

The math is brutal.

Say you start with $500,000 in annual PPO write-offs, costs rise 3% a year, and PPO fees fall 3% a year. After 10 years:

- Your costs have risen 34%

- Your PPO reimbursements have fallen 26%

- Your effective PPO loss is now 60% higher than when you started

You’re literally getting poorer every year you stay in these contracts.

Saturated Markets Make Things More Difficult

Market saturation makes everything worse. When you first joined PPO networks, fewer dentists participated.

Now? Every dentist within 10 miles takes the same plans. Competition for the same insurance patients drives everyone toward the lowest common denominator.

PPO companies know this. They’re not stupid. They sign up as many dentists as possible, then squeeze fees because they know you’ll compete with each other for patients.

You’ve become replaceable.

The career-long impact is staggering. One dentist I spoke with ran these numbers for his own practice and nearly had a heart attack. Over an expected 25-year career, assuming a modest 3% annual fee cut and 3% cost inflation, the projection looked like this:

- Total PPO write-offs: $18.2 million

- Added costs from administrative burden: $6.8 million

- Opportunity costs from reduced capacity: $4.1 million

- Projected career-long PPO cost: $29.1 million

Now, that’s a projection, not a guarantee. Markets shift, contracts change, and no two practices compound the same way.

But even if the real number lands at half of that, it’s still life-changing money.

As he put it: “I’m not just giving away money. I’m giving away my retirement, my kids’ college funds, and my family’s financial security. For what? The privilege of being on insurance panels that treat me like a commodity?”

The Retirement Crisis

The retirement crisis among dentists isn’t an accident. It’s the predictable result of 30 years of declining PPO reimbursements. Dentists who started before managed care could retire comfortably on a practice sale.

Today’s PPO-dependent dentists work into their 70s because they can’t afford to stop.

Here’s the compound effect most dentists miss: every year you wait to fix this, the solution gets harder and more expensive.

Year one of PPO dependency is easy to reverse. Year ten takes significant change. Year twenty? You might be too financially dependent on insurance revenue to survive the transition.

The patients, staff, and systems you build around PPO volume get harder to change as time passes. Your reputation becomes “the insurance dentist.”

Your referral patterns lock in. Your practice value drops.

Time is not on your side.

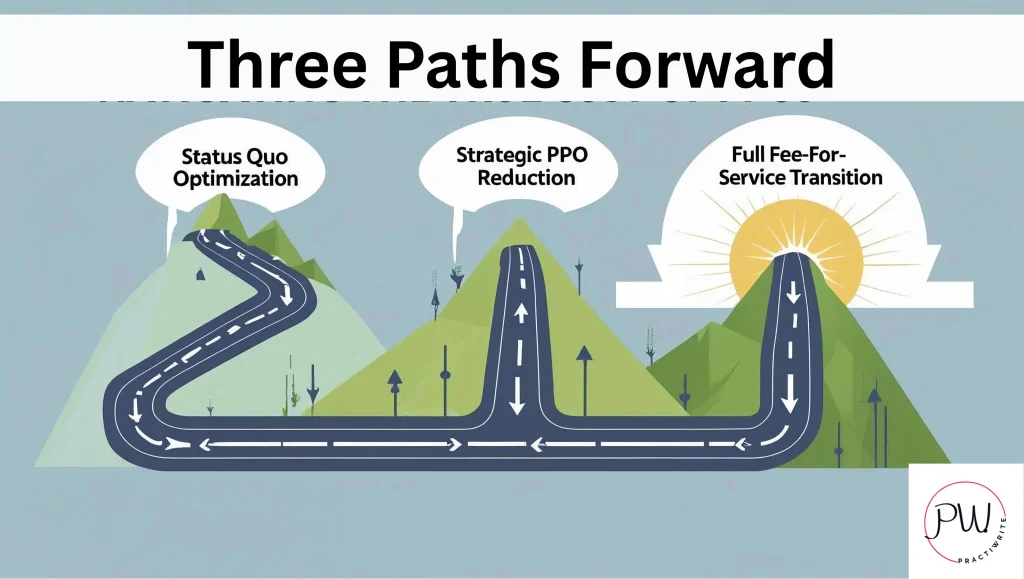

Three Paths Forward: Your Options Explained

You’ve seen the numbers. You know what PPO participation is really costing you. Now what?

You have three choices. None are perfect, but one of them will save your practice and your sanity. The others just slow the bleeding.

Path 1: Status Quo Optimization

This is the “make PPOs work better” approach. You stay in your current contracts but build systems to limit the damage. What it looks like:

- Streamline admin processes to cut hidden costs

- Negotiate better terms where possible (spoiler: this rarely works)

- Focus on efficiency to see more patients in less time

- Maximize case acceptance on covered procedures

The upside? It’s safe.

No dramatic changes. No patient loss. No scary transitions.

The downside? You’re polishing the deck chairs on the Titanic.

PPO contracts keep squeezing every year. The compound effect still destroys you over time. You might cut your annual PPO costs from $500,000 to $400,000, but you’re still giving away hundreds of thousands a year.

Best case, you buy yourself 2-3 years before the pressure becomes unbearable again. This isn’t a solution. It’s a delay tactic.

Path 2: Strategic PPO Reduction

This is the surgical strike. You keep the contracts that actually make sense and cut the ones bleeding you dry. What it looks like:

- Audit every PPO contract for true profitability

- Drop the 20% of contracts causing 60% of your problems

- Use the freed capacity for fee-for-service patients

- Gradually reduce dependency over 12-24 months

The upside? Lower risk than going full fee-for-service.

You keep some insurance patients for stability while improving margins. Most practices can pull this off without major disruption. The math: if you’re currently 85% PPO and drop to 50% over 18 months, you could see 30-40% profit increases while working fewer hours.

The downside? You’re still playing the insurance game, just with better rules. The remaining contracts keep cutting fees every year.

You’ll always be partly dependent on insurance companies. This path fits dentists who want real improvement without revolutionary change.

It’s the middle ground most practices should at least consider.

Path 3: Full Fee-for-Service Transition

This is the nuclear option. You drop all PPO contracts and build a practice based entirely on fee-for-service patients. What it looks like:

- A 12-24 month planned exit from all insurance networks

- A complete repositioning and marketing overhaul

- Focus on premium care, premium experience, premium outcomes

- A patient base that chooses you for expertise, not insurance coverage

The upside?

- Maximum profit potential

- Complete clinical autonomy

- No administrative burden

- Work-life balance

- Professional satisfaction

- Practice value maximized

Practices that transition well typically see 50-100% profit increases within 24 months, despite 20-30% revenue reductions.

The downside? Highest risk. Significant patient loss during the transition. It takes real marketing investment and practice change. And not every market can support a full fee-for-service practice.

This path fits dentists willing to bet on themselves, their skills, and their ability to deliver value patients will pay for directly.

The risk assessment, path by path:

- Status quo: low short-term risk, high long-term risk. The certainty of slow decline.

- Strategic reduction: moderate risk, moderate reward. Sustainable improvement with some ongoing insurance dependency.

- Fee-for-service: high short-term risk, highest long-term reward. Maximum freedom and profit potential.

Timeline matters too. Status quo optimization takes 3-6 months to implement. Strategic reduction takes 12-24 months for full execution.

A fee-for-service transition can take 18-36 months depending on your market and positioning. The critical factor isn’t which path you choose. It’s that you choose one.

Staying on your current trajectory guarantees continued decline.

Which path fits your practice, your market, and your risk tolerance? That depends on your answers to some honest questions about where you stand today.

The Self-Assessment: Know Where You Stand

Most dentists lie to themselves about PPO profitability. They look at gross revenue instead of net profit.

They ignore hidden costs. They rationalize bad decisions because the truth is uncomfortable.

Stop lying. Your financial future depends on brutal honesty about where you really stand. Here are the questions that tell you everything.

Financial Reality Check

What’s your actual profit per PPO patient versus a fee-for-service patient? Don’t guess. Calculate it.

Include everything: lab fees, staff time, materials, admin burden, opportunity costs. Most dentists discover their PPO patients generate 60-70% less profit than they thought.

If you don’t know these numbers, you’re flying blind. Get them. Now.

How many extra hours a week does PPO participation cost you? Track admin time, phone calls, documentation, and appeals for one month.

The average PPO practice spends 15-20 hours a week on insurance tasks that generate zero revenue. That’s 800-plus hours a year you could spend on patient care, practice development, or having a life.

Market Position Assessment

Can your market support fee-for-service dentistry? Look around.

Are there successful fee-for-service practices in your area? What do they charge? How busy are they?

If nobody in your market can make fee-for-service work, that tells you something important about your options.

What share of your new patients chooses you for your expertise versus your insurance participation? Be honest.

When patients call, do they ask about your qualifications or about whether you take their insurance? If coverage is the main driver of patient selection, you’re a commodity provider, not a healthcare professional.

Professional Satisfaction Evaluation

When did you last recommend the best treatment option without first checking coverage? If you can’t remember, you’ve let insurance companies take over your clinical decisions.

How many procedures do you avoid discussing because you know insurance won’t cover them? Cosmetic dentistry? Premium materials? Advanced techniques?

Every limitation you accept for insurance approval chips away at your autonomy.

What’s your stress level on a typical Monday morning? If the thought of another week of insurance hassles, rushed appointments, and admin burden makes you want to stay in bed, you’re burning out. Do you feel like a doctor or a technician?

Insurance-driven practices turn skilled professionals into production workers. If you’re going through the motions instead of practicing medicine, something’s wrong.

Growth Potential Analysis

Where will your practice be in five years if nothing changes? Factor in annual PPO fee cuts, rising costs, and market saturation. Most PPO practices are slowly declining even when they look busy.

What happens if your largest PPO contract drops you tomorrow? If the answer is “financial disaster,” you’re too dependent on insurance companies.

Could you survive a 30% patient loss during a transition? Fee-for-service transitions require reserves and the ability to ride out a temporary revenue dip. If you’re living paycheck to paycheck, build stability before you make major changes.

The honest scorecard:

- Profitable per PPO patient and satisfied with your autonomy? Status quo optimization might work short-term.

- Marginally profitable but burning out from volume and admin? Strategic PPO reduction is probably your best bet.

- Losing money on PPO patients or completely miserable with insurance-driven care? A fee-for-service transition is worth the risk.

The worst position? Knowing you’re losing money and satisfaction but being too scared to change.

That’s not a business strategy. That’s slow suicide.

Most dentists never ask these questions honestly because they’re afraid of the answers. But ignorance isn’t bliss when your practice is quietly bleeding to death.

You deserve better than spending your career subsidizing insurance companies while sacrificing your satisfaction and your security.

Wrapping Up: Your Practice Is Worth More Than What PPOs Are Paying

Let’s cut through all of it. PPO participation costs you more than you think.

Not just the obvious fee cuts, bad as those are. It’s the hidden admin costs, the opportunity costs, the loss of professional autonomy, and the compound effect that gets worse every year.

You’re not failing as a dentist. The system is rigged against you.

Insurance companies designed PPO contracts to extract maximum value from your expertise while paying you minimum fees. They get rich while you work harder for less.

That “successful” practice with the packed schedule and high revenue? Often a mirage. Factor in the real costs, admin burden, equipment wear, staff turnover, opportunity cost, lost autonomy, and many “busy” practices are barely breaking even. Some are losing money.

You have options.

Status quo optimization if you want to minimize short-term disruption.

Strategic PPO reduction if you want significant improvement without revolution.

Full fee-for-service if you’re ready to bet on yourself.

The choice isn’t whether to address this. It’s which solution fits your situation and your risk tolerance.

Here’s your move in the next 7 days:

- Day 1-2: Calculate your real PPO costs. Track every admin minute, every write-off, every hidden expense. Get the actual numbers, not your estimates.

- Day 3-4: Audit your PPO contracts. Which are bleeding you dry? Which might actually be profitable? Most practices find 20% of their contracts cause 60% of their problems.

- Day 5-6: Assess your market. Can your area support fee-for-service dentistry? What are the successful non-PPO practices near you doing differently?

- Day 7: Decide. Status quo, strategic reduction, or full transition. Pick a path and commit. Indecision is the most expensive choice you can make.

The longer you wait, the harder this gets. Every year of PPO participation locks you deeper into insurance dependency.

Every year of reduced fees compounds into bigger losses. Every year of admin burden and rushed care chips away at your satisfaction.

You didn’t spend eight years in dental school to become an insurance processor. Your practice is worth more than what insurance companies pay. Your time is worth more than what PPO contracts allow.

Your expertise deserves better than rushed appointments and treatment limits.

Ready to take control of your practice’s future?

Here’s the part nobody connects for you. The moment you decide to lean away from PPOs, one thing has to be true: patients have to choose you for your expertise, not because your name shows up on their insurance card.

So what makes them choose you? What they find when they search.

Your Google Business Profile and your website are the front door to a fee-for-service practice. They’re the difference between a steady stream of patients who pay full fee and crickets.

Before you drop a single contract, you need to know whether your online presence can actually pull in the patients who’ll replace that PPO volume.

That’s exactly what we look at first.

Schedule your 100% free Dental Practice Roadmap. Your Dental Practice Roadmap is a GBP and website audit that shows you exactly where you stand, what keywords you’re ranking for now, what you should be ranking for, and a step-by-step plan to close those gaps.

No vague recommendations. No fluff. Just a clear picture of what’s broken and what to do about it.

Book your Dental Practice Roadmap and get yours today now.

10+ year content strategist, writer, author, and SEO consultant. I work exclusively with dental practices that want to grow and dominate their local areas.