A fee-for-service dental practice transition is the staged process of dropping insurance contracts while rebuilding your patient base around people who choose you on purpose.

It usually takes 12 to 24 months. Done right, you set your own fees, treat based on clinical need, and get paid directly. Done wrong, you watch your schedule empty out.

Here’s the part most consultants skip. The practices that survive this transition are the ones who fix their visibility before they drop plans, not after.

Insurance companies have been tightening the screws for years.

Reimbursements drop.

Admin demands climb.

You see more patients to earn the same money.

And the PPO contracts you signed to “guarantee patient flow” now dictate your fees and your treatment plans.

You already know this. In its Q4 2025 State of the U.S. Dental Economy report, the ADA Health Policy Institute found that dentists followed through on nearly every business plan they set for the year.

Nearly every one, except dropping out of insurance networks. That was the goal most of them quietly gave up on.

Why? Because leaving insurance feels like jumping without a net.

It isn’t.

It’s a system with predictable steps and predictable outcomes. This guide walks you through all of them, including the one nobody talks about: what happens to your new patient flow the day you leave the network.

Table of Contents

What Is a Fee-For-Service Dental Practice Transition?

A fee-for-service dental practice transition is the move from billing insurance networks to billing patients directly for the care you provide. In a fee-for-service model, the financial relationship is between you and your patient.

They pay your fee. Insurance, if it’s involved at all, reimburses the patient, not you.

You’re not bound by network fee schedules. You’re not bound by coverage policies that call a necessary crown “cosmetic.” You set fees based on your real costs and the value you deliver.

So why do so many practices stay stuck? Because they think the only choice is all-in or all-out. It isn’t.

What’s the Difference Between FFS and PPO Practices?

A PPO practice runs on volume. A fee-for-service practice runs on quality. That’s the whole difference in one line.

In a PPO practice, insurance contracts set your fees, coverage rules limit your treatment options, and your front desk burns hours on verification, pre-authorization, and claims. Payment shows up in 30 to 90 days, minus the write-offs.

In a fee-for-service practice, you set the fee. Treatment is based on what the patient needs. Payment lands at the time of service.

There’s no write-off and no pre-authorization delay. Fewer patients, more time per patient, more revenue per chair. To see exactly what staying in-network costs you, read the true cost of PPO participation.

What Are the Three FFS Transition Models?

There are three ways to structure a fee-for-service practice, and you don’t have to pick the most aggressive one.

Pure fee-for-service

Patients pay your full fee at the time of service. You don’t file claims. They handle their own reimbursement.

Lowest admin load, but it works best with patients who are comfortable paying upfront.

Courtesy billing

You file the claim as a favor to the patient, but they still pay your full fee at the time of service. The insurance reimbursement goes to them. You get convenience for the patient and cash flow protection for the practice.

Hybrid

You drop your worst-reimbursing, highest-hassle plans and keep a small number that still make sense. Most practices use this as the on-ramp, shrinking insurance dependence over 12 to 24 months.

Is Your Practice Actually Ready to Drop Insurance?

A practice is ready for a fee-for-service transition when it understands its true numbers, knows which patients will stay, and operates in a market that can support out-of-pocket care. Readiness isn’t a feeling. It’s three concrete things you can measure this month.

Skip this step and you’re guessing. Guessing is how transitions fail.

How Do You Audit Your Insurance Contracts?

Auditing your contracts means calculating what you actually keep from each plan, not what you bill. Divide your real collections by your total production for each insurance plan. Then subtract the hidden costs: staff hours spent on verification, pre-auth, claims, and chasing denials.

Most dentists are stunned by what’s left. When you fold in write-offs and admin time, it’s common to net far less than your real fee for the same procedure.

The plans you think are “fine” are often the ones bleeding you. Once you see the true number, setting fees that reflect your real costs gets a lot easier.

Which Patients Will Follow You, and Which Won’t?

Your patients sort into three groups, and only two of them matter for this decision. There are the patients who consistently accept comprehensive care. The patients who sometimes do. And the patients who only ever want what insurance covers.

The first group will follow you. They already value your work. The third group probably won’t, and that’s fine.

A transition isn’t about keeping every patient. It’s about keeping the right ones. For a deeper look at this, see whether your patient base is ready for a fee-for-service model.

Does Your Local Market Support Fee-for-Service?

Your market supports fee-for-service when patients have discretionary income and already pay out of pocket for quality services. Look at median household income, education levels, and whether other fee-for-service practices are thriving nearby.

Competitors succeeding in your area isn’t bad news. It’s proof the model works where you are.

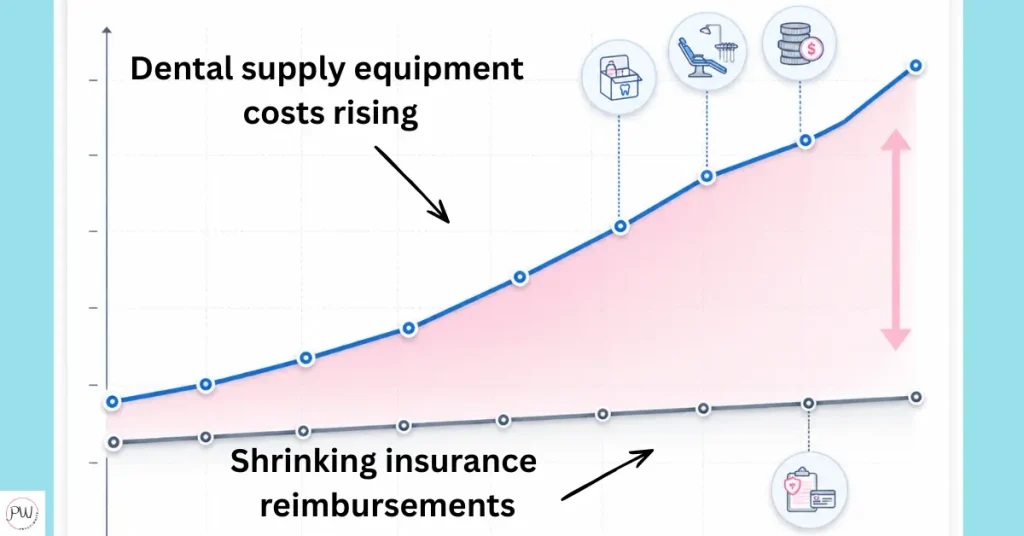

There’s a headwind to plan around, though. The ADA Health Policy Institute reported in 2025 that the prices dentists pay for supplies, equipment, and staff wages are climbing faster than insurance reimbursement rates.

The ADA has a name for it. They call it the fiscal squeeze. That gap is exactly why staying in-network gets more painful every year, and why the math for transitioning keeps getting better.

How Do You Transition From PPO to Fee-for-Service?

You transition from PPO to fee-for-service by dropping plans in stages over 12 to 24 months while protecting cash flow at every step. Nobody announces it Monday and implements it Tuesday.

The practices that succeed follow a sequence. Here it is.

Step 1: Build Your Timeline and Cash Reserves

Start by mapping which plans you’ll drop and when. Begin with your lowest-reimbursing, highest-hassle contracts. Plan to drop one plan every three to four months, with a checkpoint every quarter.

Before you drop anything, build a cash reserve that covers four to six months of operating expenses. This is the cushion that keeps you from panicking and reversing course the first time cash flow tightens. Practices that transition without reserves almost always retreat.

My month-by-month checklist for leaving PPOs lays the timeline out for you.

Step 2: Set Fees That Reflect Your Real Costs

Build a fee schedule from your actual numbers:

- Overhead

- Materials

- Lab costs

- The income you need

- And a real profit margin

Many practices discover their insurance-contracted fees never covered their true costs in the first place.

Research local rates, but don’t just copy them. If you deliver better care with better materials and more time, your fees should say so.

You’re not trying to be the cheapest. You’re trying to be the clear best value.

Step 3: Train Your Team to Talk About Value

Your team’s ability to talk about value, not coverage, decides whether this works. Insurance-trained staff lead with “here’s what your plan covers.” Fee-for-service staff lead with “here’s what your health needs.”

Write scripts for the conversations that happen every day: presenting treatment cost, handling a price objection, explaining out-of-network benefits. Then role-play them until they feel natural. Teach your team to reframe cost in plain terms.

A $1,200 crown that lasts 15 years is about $7 a month to keep a tooth. Patients understand value. They struggle with sticker price.

Step 4: Notify Patients With a 90-Day Runway

Give patients at least 90 days of notice before you drop their plan. Send a written letter that explains the change, the reason behind it, and what they gain. Follow up by phone with your highest-value patients so they hear it from a person.

Frame it around what improves: longer visits, better materials, no pre-authorization delays, treatment based on their needs. And make this clear, because most patients don’t know it: they can still use their benefits. The reimbursement just comes to them instead of to a discounted contract.

For the exact language, see how to tell patients you’re dropping insurance.

Step 5: Drop Plans One at a Time and Monitor Weekly

Drop your first plan, then watch the numbers weekly. Not monthly. Track patient retention, new patient requests, production per patient, and cash flow. Weekly review catches problems while they’re still small.

If retention holds and cash flow stays stable, drop the next plan on schedule. If retention drops below your floor, slow down. The pace is yours to control. That’s the whole point of doing it in stages. For a full month-by-month view, see my PPO to fee-for-service transition timeline.

What Replaces Dental Insurance for Your Patients?

When you leave insurance networks, three proven tools replace it for your patients: membership plans, financing, and cash discounts.

The myth is that patients lose all financial help when you go out of network. They don’t. They trade a broken system for options that actually work.

Would your patients rather have “coverage” that caps at the same dollar amount it did in the 1970s, or a plan with no annual maximum at all? When you put it that way, the conversation changes.

How Do Membership Plans Work?

A membership plan is a subscription patients buy directly from your practice. They pay an annual fee, usually a few hundred dollars, and get their preventive care plus a set discount on other treatment.

No deductibles. No annual maximums. No waiting periods.

For you, it’s predictable recurring revenue and a patient base that’s committed because they’ve prepaid for care. Platforms like Kleer, BoomCloud, and Dental HQ handle the enrollment and billing for a small cut, so it doesn’t add to your front desk load. For help deciding between approaches, see membership plans versus financing.

What Financing Options Should You Offer?

Offer a mix of in-house payment plans and third-party financing so cost is never the reason a patient says no. For smaller cases, short no-interest plans with a real down payment work well. For larger cases, third-party partners like CareCredit pay your practice within a few business days and give the patient longer terms.

The approval takes minutes and patients can apply before the appointment. That moves the awkward money talk out of the treatment chair entirely.

Are Cash Discounts Legal?

Yes, cash discounts are legal in every state when you structure them as a true discount for payment at the time of service, not a surcharge for other payment types. The distinction matters legally and it matters to patients.

Offer a small discount, often 3 to 5%, for payment by cash, check, or debit at the time of service. Base the percentage on what you’d otherwise lose to card processing fees. Check your state’s specific rules and your merchant agreement first, and put the policy in writing so your team explains it the same way every time.

Why Do Most Fee-for-Service Transitions Stall?

Most fee-for-service transitions stall at one of three predictable points: patient resistance, cash flow pressure, or staff pushback.

The challenges aren’t a surprise. The practices that fail are the ones who didn’t plan for them. The practices that succeed treat them as speed bumps, not stop signs.

How Do You Handle Patient Resistance?

Handle patient resistance with education, because resistance almost always comes from misunderstanding, not from a real objection to your value. Many patients think their dental insurance is generous. Most don’t realize the annual maximum hasn’t meaningfully moved in decades while dental costs have climbed every year.

Show them the gap in plain terms. Use real examples where coverage rules forced a compromise.

And here’s the part that surprises most dentists: your loyal, high-value patients usually support the change. The resistance comes from the patients who were never really yours to begin with.

How Do You Protect Cash Flow During the Transition?

Protect cash flow by building reserves before you start and modeling the worst case before it happens. Assume a real chunk of patient attrition in the first six months and plan your budget around the lower number. Clean up your accounts receivable before you drop a single plan, so you enter the transition with your books tight.

A line of credit, set up while your practice still looks strong on paper, is cheap insurance. You may never touch it. But knowing it’s there is what keeps you from reversing course at the first slow week.

How Do You Get Your Team on Board?

Get your team on board by addressing the fear directly: insurance-heavy staff worry their jobs disappear when the insurance work does.

So show them where the work goes. Your insurance coordinator becomes your patient care coordinator. The hours once lost to hold music get spent on patient education and treatment coordination.

Bring the team into the planning. People implement systems they helped build. They resist systems handed to them.

And keep them updated on how the transition is actually going, because silence breeds anxiety faster than bad news does.

What Happens to Your New Patient Flow When You Leave PPOs?

When you leave a PPO network, you also leave its patient referral pipeline, and most practices have no plan to replace it. This is the step nobody talks about, and it’s the one that quietly sinks transitions.

Your clinical plan can be perfect. Your fee schedule can be perfect. But if new patients can’t find you, none of it holds.

Here’s the number that should stop you cold. In the ADA Health Policy Institute’s Q4 2025 report, one-third of dentists said they weren’t busy enough. A year earlier, it was one-quarter. And that’s happening while consumer spending on dental care rose 4% over the same twelve months.

Demand went up. Visibility didn’t. That gap is the whole problem.

Why Does Your Google Business Profile Matter More After You Go FFS?

Your Google Business Profile matters more after you go fee-for-service because it becomes your primary patient pipeline once the insurance directory listing is gone. PPO patients used to find you through the insurer’s “find a dentist” tool. Fee-for-service patients find you on Google.

That means your profile, your reviews, and your local search visibility aren’t a marketing nice-to-have anymore. They’re the replacement for the referral channel you just gave up. Fix this before you drop plans, not after.

Start with how to rank your dental practice in the Google Maps pack.

How Do Fee-for-Service Patients Actually Find and Choose a Practice?

Fee-for-service patients find practices through search and choose them through reputation. They’re not picking from an insurance list. They’re researching, and they’re pickier than they used to be.

BrightLocal’s 2026 Local Consumer Review Survey found that 68% of consumers will only use a business rated four stars or higher. A year earlier, that was 55%. The bar is rising fast.

The same survey found that the share of consumers using AI tools like ChatGPT for local recommendations jumped from 6% to 45% in a single year. The patients you want are searching in new places, and they’re judging you before they ever call.

This is exactly what fee-for-service dental marketing is built to solve, and it’s the core of patient generation for FFS dentists.

How Do You Start Your Fee-for-Service Transition This Week?

You start your fee-for-service transition this week by making three concrete moves, none of which involve dropping a plan yet. Most dentists research this decision for months and never take a first step.

Movement creates momentum. Here’s where to put it.

Move One: Run The Contract Math

Pull 12 months of reports. Calculate your true reimbursement rate per plan, write-offs and admin time included. Let the numbers tell you which contracts actually earn their place.

Move Two: Segment Your Patients

Sort your active patients into the three groups from earlier. You’ll see immediately how much of your base is already fee-for-service in everything but name.

Move Three: Audit Your Visibility

Search “dentist near me” in your town. Look at your Google Business Profile, your reviews, your ranking. If you can’t be found now, with insurance still feeding you patients, that’s the gap to close first.

Which of those three could you finish before Friday?

Frequently Asked Questions

Still have questions? Let’s get some answers:

What does it cost to transition a dental practice to fee-for-service?

The main cost of a fee-for-service transition is the temporary revenue dip during patient attrition, not a fee paid to anyone. Practices typically plan for a cash reserve covering four to six months of operating expenses to bridge the transition. Direct costs are minor and include items like patient communication materials, team training, and payment processing or membership plan platform fees.

How long does a PPO to fee-for-service transition take?

A PPO to fee-for-service transition typically takes 12 to 24 months. Most successful practices drop one insurance plan every three to four months, starting with the lowest-reimbursing contracts, and monitor financial results between each step. A faster timeline is possible in strong markets but requires larger cash reserves.

How many patients will I lose when I drop insurance?

Most practices see patient attrition during the first six months of a fee-for-service transition, concentrated among patients who only accept insurance-covered treatment. High-value patients who already accept comprehensive care tend to stay. Conservative financial planning assumes a meaningful attrition rate and budgets around the lower revenue number.

Can patients still use their insurance at a fee-for-service practice?

Yes. Patients with dental benefits can still use them at an out-of-network fee-for-service practice. The difference is that the insurance company reimburses the patient directly rather than paying the practice a discounted contracted rate. Many practices offer courtesy billing, where the practice files the claim on the patient’s behalf while still collecting the full fee at the time of service.

How do I handle dental emergencies in a fee-for-service practice?

Fee-for-service practices handle emergencies with clear, written policies for urgent care and new patient situations, often paired with financing options for unexpected treatment. Setting these policies before the transition prevents confusion at the front desk. For a full breakdown, see my blog on emergency dental care in a fee-for-service practice.

Wrapping Up: The Transition Works. The Order Is What Most Practices Get Wrong.

Here’s what you now know that most dentists don’t. A fee-for-service transition isn’t a leap of faith. It’s a sequence.

You audit your contracts, you find the patients who already value you, you build reserves, you drop plans in stages, and you replace insurance with options that actually serve your patients.

But there’s one step that decides whether the whole thing holds. When you leave a network, you leave its patient pipeline.

If you haven’t built your own before that day, you’re transitioning into an empty schedule. The dentists who succeed don’t just plan the exit. They fix their visibility first.

That’s the move to make now, while insurance is still feeding you patients and you have room to get it right.

Or let Practiwrite handle it with you.

Schedule your 100% free Dental Practice Roadmap. Your Dental Practice Roadmap is a GBP and website audit that shows you exactly where you stand, what keywords you’re ranking for now, what you should be ranking for, and a step-by-step plan to close those gaps.

No vague recommendations. No fluff. Just a clear picture of what’s broken and what to do about it.

Book your Dental Practice Roadmap and get yours now.

10+ year content strategist, writer, author, and SEO consultant. I work exclusively with dental practices that want to grow and dominate their local areas.